Audit of Governance

Table of contents

Executive Summary

The objective of this audit was to assess whether Public Safety Canada’s internal governance structure operates effectively and provides oversight over key departmental activities.

The scope of this audit included the review and assessment of all records and processes relevant to Public Safety Canada’s internal governance structure that were in place from April 2017 to November 2018.

This includes the following governance bodies: Departmental Management Committee, Internal Policy Committee, Executive Committee, Director Generals Management Committee, Committee for Collective Management of Human Resources, and Performance Measurement and Evaluation Committee.

Why is this important?

Pursuant to the Financial Administration Act, deputy heads are responsible for organizing the department’s resources in order to deliver departmental programs in compliance with government policies and procedures as well as for the measures taken to maintain effective systems of internal control in the department. This is accomplished namely through the establishment of an appropriate governance structure that provides support to the deputy head and senior management in the achievement of departmental objectives.

Departments must thus establish an effective governance structure based largely on the specific operational context of the organization as well as generally accepted management practices. The governance structure and processes must be assessed regularly to ensure continued alignment with departmental priorities and objectives as well as operational efficiency and effectiveness.

Pursuant to the International Standards for the Professional Practice of Internal Auditing, the Department’s internal audit function supports the deputy head in this responsibility by assessing and making appropriate recommendations to improve the organization’s governance processes, namely to ensure effective organizational performance management and accountability as well as strengthen the organization’s ability to make strategic and operational decisions.

Key Findings

The audit found that Public Safety Canada’s governance bodies have documented terms of reference that include key elements defining their general objective; however, further clarity over their mandate, purpose and scope would help ensure continued alignment with departmental objectives and management expectations. Clear and precise committee terms of reference contribute to ensuring that decisions are made following a consistent, transparent and established process that is based on documented and agreed-upon responsibilities and accountabilities.

We expected the governance structure established at Public Safety Canada to operate effectively and ensure oversight and decision-making over all key departmental activities, in support of the Department’s overall mandate and expected results. We found that the Department has governance bodies in place to support decision-making over all key departmental activities; however, there is no process for regular and overarching review of the governance structure and governance bodies’ terms of reference to support comprehensive oversight and effective decision-making.

Conclusion

Public Safety Canada has established governance bodies that operate in compliance with their terms of reference and provide oversight over key departmental activities. However, improvements can be made to clarify elements of the terms of reference and increase effectiveness of the governance structure.

Recommendation

The governance bodies’ secretariats, at the direction of the committees’ Chair and Members, should establish an integrated governance framework that:

- supports departmental objectives and is reviewed regularly to ensure continued alignment with senior management expectations.

- Is composed of governance bodies that have terms of reference clearly defining the following key elements:

- Mandate

- Purpose, including decision-making authority

- Scope

- Membership/Composition

- Roles and responsibilities

- Quorum requirements

- Frequency of meetings

- Regular review of the terms of reference.

1. Introduction

1.1 Background

Governance in the federal public administration

Pursuant to the Financial Administration Act, deputy heads are responsible for organizing the department’s resources in order to deliver departmental programs in compliance with government policies and procedures as well as for the measures taken to maintain effective systems of internal control in the department. This is accomplished namely through the establishment of an appropriate governance structure that provides support to the deputy head and senior management in the achievement of departmental objectives.

While there are no legislative or Treasury Board requirements that specifically prescribe the appropriate governance structure for departments, the expectations for sound organizational performance are outlined as part of the Management Accountability Framework (MAF). One element of the MAFis Governance and Strategic Management, which is defined as the organization’s ability to maintain effective governance that integrates and aligns priorities, plans, accountabilities and risk management to ensure that internal management functions support and enable high performing policies, programs and services.

Furthermore, industry best practices, such as the Committee of Sponsoring Organizations of the Treadway Commission (COSO) Internal Control Integrated Framework, provide guidance to management on the implementation of effective risk management and internal control processes, leading to the improvement of management and governance processes. When applied effectively, the framework’s concepts contribute to effective organizational performance and governance.

Departments must thus establish an effective governance structure based largely on the specific operational context of the organization as well as generally accepted management practices. The governance structure and processes must be assessed regularly to ensure continued alignment with departmental priorities and objectives as well as operational efficiency and effectiveness.

Pursuant to the International Standards for the Professional Practice of Internal Auditing, the Department’s internal audit function supports the deputy head in this responsibility by assessing and making appropriate recommendations to improve the organization’s governance processes, namely to ensure effective organizational performance management and accountability as well as strengthen the organization’s ability to make strategic and operational decisions.

Governance at Public Safety Canada

Public Safety Canada has established a number of governance bodies that support the department’s mandate and objectives, both internally and from a portfolio perspective. Senior management and employees at all levels also actively participate in numerous interdepartmental or federal/provincial/territorial governance bodies on a wide variety of topics relevant to Public Safety Canada’s mandate.

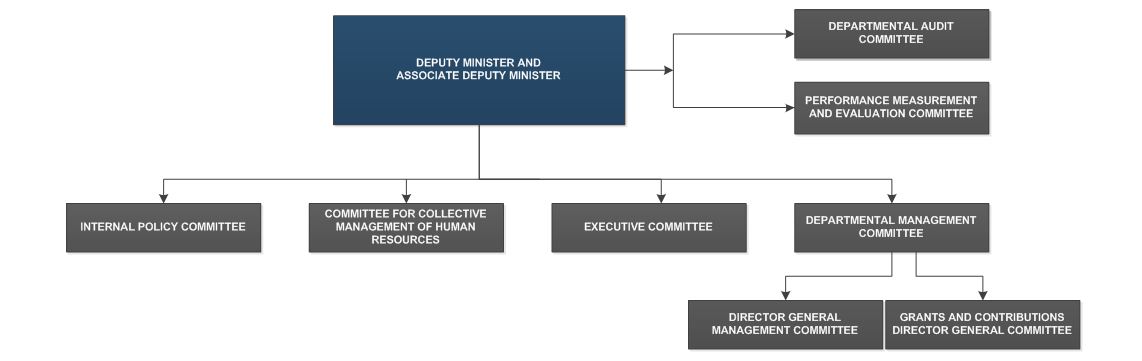

At the time of the audit, Public Safety Canada’s internal governance structure was comprised of eight main senior-level committees, as represented in Figure 1 below.

Figure 1: Public Safety Canada’s Internal Governance Structure

Image Description

Figure 1 illustrates the Department’s internal Governance Structure. The organizational chart depicts the four internal committees chaired by the Deputy Minister and for which the membership is mainly comprised of individuals at the Assistant Deputy Minister level. These committees are (from left to right) the Internal Policy Committee, the Committee for Collective Management of Human Resources, the Executive Committee and the Departmental Management Committee (DMC). Reporting to DMC are the Grants and Contributions Director General Committee and the Director General Management Committee. Pursuant to Treasury Board Policies, Performance Measurement and Evaluation Committee and the Departmental Audit Committee also figure on the organization chart. They are comprised of the Deputy Minister, Associate Deputy Minister, Assistant Deputy Ministers and external members.

Public Safety Canada has established four internal governance bodies chaired by the Deputy Minister and for which the membership is mainly comprised of individuals at the Assistant Deputy Minister level:

- Departmental Management Committee (DMC): Provides oversight and makes decisions on management issues regarding the department’s operation and direction in the areas of financial management, human resources management and general management.

- Internal Policy Committee (IPC): Considers key policy issues and provides the Deputy Minister with integrated strategic advice on draft Departmental Memoranda to Cabinet (MC) and relevant draft Portfolio MCs.

- Committee for Collective Management of Human Resources (CCMHR): Is a senior executive decision forum where human resources issues can be discussed and addressed with a corporate lens.

- Executive Committee (Excom): Serves as a weekly forum for the Deputy Minister and Associate Deputy Minister to provide strategic direction, debrief on meetings, receive updates and review the departmental agenda. It is a planning venue that allows for exchanges on short-term priorities.

Two committees comprised of the Deputy Minister, Associate Deputy Minister, and Assistant Deputy Ministers are also in place pursuant to legislation and/or policy requirements:

- Performance Measurement and Evaluation Committee (PMEC): Supports the Deputy Minister in overseeing the performance measurement and evaluation functions of the Department and the use of performance measurement and evaluation information in decision-making. PMEC are established government-wide pursuant to the Treasury Board Policy on Results. Public Safety Canada has an external member serving on the PMEC, which is chaired by the Deputy Minister. At the time of the audit, secretariat support for PMEC was jointly provided by the Internal Audit and Evaluation Directorate (IAED) and the Portfolio Affairs and Communications Branch (PACB).

- Departmental Audit Committee (DAC): Provides objective advice and recommendations to the Deputy Minister regarding the sufficiency, quality and results of internal audit engagements related to the adequacy and functioning of the Department's framework and processes for risk management, control and governance. DACs are established in departments government-wide pursuant to the Financial Administration Act and the Treasury Board Policy on Internal Audit and are comprised of a majority of members from outside the federal public administration. Public Safety Canada’s DAC is chaired by an external member.

- Grants and Contributions (G&C) Director General Committee: Provides leadership and acts as an advisory and oversight body for G&C management.

- Director General Management Committee (DGMC): Allows for Director General-level consultations, deliberation, and challenge function on general management issues prior to presenting to the DMC. DGMC can also approve operational management matters that do not require DMC approval.

The DGMC was disbanded in 2019 to establish the Resource Management Committee (RMC), which is tasked specifically with reviewing the development, integration, and implementation of departmental processes, reports and plans for corporate resources. The RMC is chaired by the Associate Deputy Minister and reports to the DMC.

1.2 Audit Objective and Scope

The objective of this audit was to assess whether Public Safety Canada’s internal governance structure operates effectively and provides oversight over key departmental activities.

For the purpose of this audit, ‘’departmental activities’’ are defined as Public Safety Canada’s Core Responsibilities under the Departmental Results Framework (including internal servicesFootnote1). We also assessed whether the governance structure in place effectively supports oversight and decision-making related to strategic planning, organizational performance management, and values and ethics.

The scope of this audit included the review and assessment of all records and processes relevant to Public Safety Canada’s internal management governance structure that was in place from April 2017 to November 2018. This includes the following governance bodies: Departmental Management Committee, Internal Policy Committee, Executive Committee, Director General’s Management Committee, Committee for Collective Management of Human Resources, and Performance Measurement and Evaluation Committee.

The scope did not include:

- The governance structure that supports Public Safety Canada’s portfolio responsibilities, i.e. interdepartmental or federal/provincial/territorial governance bodies.

- The DAC, given the external third party practice inspection that was recently completed in conformance with the Internal Auditors' International Professional Practices Framework.

- The Grants and Contributions Director General Committee, given recent coverage as part of the Internal Audit of Grants and Contributions.

- The controls in place for governance over fraud risk in the department, which were recently addressed through IAED’s consulting engagement on Enterprise Risk Management.

- Other internal Public Safety Canada governance bodies, including working groups, forums, networks and other committees not listed above, given available resources for this audit; however, linkages between these and the aforementioned governance bodies that are within the scope have been assessed where relevant to allow the audit team to appropriately conclude on its objective.

1.3 Methodology and Audit Approach

For each criteria established, an audit methodology was developed to adequately examine the area to support the objective. Methodology or approach refers to the work involved in gathering and analyzing information to achieve audit objectives. This work ensured that sufficient and appropriate audit evidence was collected to enable the audit team to draw conclusions related to each audit objective.

To complete the engagement, the following methods were used:

- Consultation with a subject-matter expert;

- Observation at committee meetings;

- Analysis;

- Interviews with relevant stakeholders; and,

- Documentation review.

IAED was not responsible for examining the effectiveness of the PMEC as part of this audit, given its role as co-secretariat for the committee. The assessment was conducted by an external auditor in order to appropriately mitigate any risk of real or perceived conflict of interest, and ensure that an independent and objective perspective is maintained. The results of this independent assessment are included in this report.

1.4 Conformance with professional standards

The audit conforms with the Institute of Internal Auditors' International Standards for the Professional Practice of Internal Auditing and the Government of Canada’s Policy on Internal Audit, as supported by the results of the Quality Assurance and Improvement Program.

2. Findings and Recommendation

2.1 Finding 1: Public Safety Canada governance bodies have documented terms of reference that include key elements defining their general objective; however, further clarity over their mandate, purpose and scope would help ensure continued alignment with Departmental objectives and management expectations.

The terms of reference is the foundational document that outlines a governance body’s mandate and associated operating procedures that supports the members in collectively achieving their shared objectives. Clear and precise committee terms of reference contribute to ensuring that decisions are made following a consistent, transparent and established process that is based on documented and agreed-upon responsibilities and accountabilities.

While terminology used may vary between organizations, governance best practices suggest that, to be effective, the terms of reference of governance bodies include the following key elements:

- Mandate: states the committee’s raison d’être and should be linked to the overarching organizational objective that it is aiming to achieve.

- Purpose: outlines the authorities and accountabilities of the committee, including whether it is advisory or has the authority to make decisions, etc.

- Scope: highlights the specific areas of management responsibility that falls within the committee’s authority, as defined in the Purpose.

- Membership: committee composition that is established based on the members collectively possessing sufficient knowledge, experience and time to discharge their mandate. In public administrations, membership is often based on the level occupied by a person in the organization as opposed to their individual qualifications.

- Roles and Responsibilities: define the expected contribution of the members and chair as well as of any other individuals supporting the committee’s operations.

- Other general operating procedures, including frequency of meetings, quorum requirements, process to disseminate meeting material and to record decisions/actions, etc.

The audit found that, with the exception of Excom, internal governance bodies at Public Safety Canada have documented terms of reference that generally include the key elements listed above. While these elements are documented, they could be further clarified to ensure a common understanding of the expectations and accountabilities for each committee.

Governance bodies with decision-making authority

The DMC is the main senior management committee responsible for oversight and decision-making over general management areas. As per its Terms of Reference dating from 2017, DMC aims to “identify strategic priorities, provide operational direction for the day-to-day management of the Department, and monitor progress made over established performance indicators and targets”. DMC also “provides oversight and makes decisions on management issues regarding the Department's operation and direction, in the areas of financial management, human resources management and general management”, with “general management” defined through a list of 17 areasFootnote2, as well as “all other internal functions” not specifically listed. DMC members are expected to review and approve “policies, projects, plans, performance, and reports relating to a broad and diverse suite of corporate management programs and services for the Department”. As such, the DMC’s decision-making authority documented in the Terms of Reference encompasses all areas of management, setting the expectations for DMC to have responsibility for approving most items supporting internal services in the Department.

At its inception in 2013, the purpose of the DGMC was to allow for consultations, deliberation and challenge function prior to presentation at the DMC, in an effort to facilitate internal engagement. The Director General of Corporate Services Directorate, Corporate Management Branch, acts as the Secretary for DMC and chairs DGMC, and is the lead executive for the Governance Secretariat responsible for both committees.

Over the course of its existence, the DGMC’s mandate was the subject of multiple revisions, namely to address challenges with members’ low attendance rate. The scope of responsibility for DGMC initially mirrored that of DMC, but was subsequently narrowed to the areas of financial management, human resources management, information technology, information management, security management and management of acquired services and assets. The committee’s responsibilities over those management areas were broadly defined as intended to support the Department by “cover[ing] program, policies, processes, systems and internal control”. The DGMC Terms of Reference was also revised in 2018 to enable the committee to “approve departmental management operational matters that do not require DMC approval”. Finally, given that senior management recognized that the decision-making process as it relates to resource expenditures was not always clear, the DGMC was disbanded and the RMC was established. The RMC, which held its first meeting in February 2019, focuses namely on DG-level of "IM-IT, HR, Finance and Procurement, and Real Property strategies, plans projects and reporting " prior to recommending for DMC approval.

In addition to DMC’s and DGMC’s (now RMC) responsibilities, the CCMHR was established to provide an opportunity for the Deputy Minister and ADMs to discuss human resource management items, namely on executive staffing, performance and talent management, leadership programs and succession planning. As per its Terms of Reference, the committee is a senior executive decision-making forum where issues can be discussed with a corporate lens, namely on the alignment of executive resources and activities to departmental objectives as well as the development and implementation of a sustainable organizational structure.

As previously noted, the PMEC was established to support the Deputy Minister in establishing and maintaining robust performance measurement and evaluation functions. The Terms of Reference for PMEC was updated in early 2019, during the course of the audit, to more closely align it with the expectations of the Policy on Results. The revision further clarified the Committee’s decision-making authority by providing specific accountability for the Chair to approve all performance measurement and evaluation products brought forward based on the recommendations of the Committee.

The audit found that the documented scopes of the governance bodies established at Public Safety Canada collectively encompass all general management areas, without limiting the extent of their respective responsibilities and decision-making authority. A clear delineation between the committees and specificity over the nature of activities for which they are each responsible would help ensure continued alignment with departmental objectives and management expectations.

Without a clear definition of DMC’s decision-making authority, DGMC’s own authority to approve was consequently difficult to define and appeared challenging to exercise. This is evidenced by the low rate of items presented for DGMC approval during the scope of the audit (12%), versus items presented for information (62%) or discussion (26%). While not within the scope of this engagement, the audit examined the Terms of Reference for the newly established RMC and noted that it more clearly defines the expectations for the committee as a recommending body to the DMC without decision-making authority.

Further, it is unclear from the CCMHR’s Terms of Reference how its mandate and decision-making authority differs from the DMC’s responsibility to “discuss human resources challenges and build on the strengths of HR programs and operations to ensure PS is a workplace of choice and has a workforce that ensure the success of its programs”. However, it should be noted that the committee members interviewed agreed that, in practice, delineation of human resources responsibilities and scope between DMC and CCMHR are clearly understood by its members.

According to their documented terms of references, the responsibilities of the PMEC and DMC also appear to overlap as it relates to monitoring Departmental performance and risk management. While the PMEC is responsible for advising the Deputy Minister on the “establishment, implementation and maintenance of the Departmental Results Framework and Program Inventory with its related Performance Information Profiles”, the DMC similarly “monitors progress made over established performance indicators and targets ”and reviews and approves policies, projects, plans and report related to performance and risk management in the Department. However, our review of records of decisions has revealed that performance information is generally discussed at PMEC, while issues related to risk management have been presented at DGMC, DAC and PMEC.

Governance bodies established for consultation or information sharing purposes

The IPC and Excom are the two senior-level committees established for the purposes of sharing information or consultation on key departmental activities.

The Excom serves as a weekly planning forum for the Deputy Minister and Associate Deputy Minister, and allows for timely exchanges and debriefings on key emerging issues. While there is no formal terms of reference for this committee, a description of its mandate is published on the Departmental Intranet. The Director General, Parliamentary and Cabinet Affairs and Executive Services within PACB acts as the Secretariat for this committee.

While the description of the Excom’s purpose speaks to the committee’s ability to “make decisions on behalf of all other committees” should need be, the Committee’s Secretariat confirmed that items are typically not presented to this committee with the intent of seeking approval. However, this weekly forum for senior management has provided opportunities for the Deputy Minister to provide direction and/or make decisions in some instances. Overall, the committee is used mainly as a venue to discuss any upcoming engagements for the Minister or Deputy Ministers, updates on key files and other short-term priorities.

The IPC is the only governance body at the Deputy Minister and Assistant-Deputy Minister levels tasked with discussing policy issues and proposals. The Strategic Policy, Research, Planning and International Affairs Directorate, PACB, is responsible for providing secretarial support to the IPC.

The audit found that items presented at IPC were consistent with the committee’s mandate to consider key departmental issues and provide the Deputy Minister with integrated advice on draft MCs. IPC serves as a forum to routinely discuss general policy matters as well as to plan and prioritize Cabinet initiatives.

While being an essential part of the committee’s purpose, the IPC Terms of Reference does not clearly define expectations as it relates to discussions on draft MCs. The Raison d’être section of the Terms of Reference states that IPC members are to provide advice on drafts Departmental MCs as well as relevant draft Portfolio MCs; however, the expectations for what constitutes relevant Portfolio MCs are not clearly defined. Furthermore, the Terms of Reference stipulates that "MCs led by Portfolio Agencies and/or other government departments would be presented by the responsible Assistant Deputy Minister"; however, it is unclear what expectations exist in this regard. In addition, the Terms of Reference stipulate that MCs should be presented “in the early to middle stages of the development process”, and again “prior to seeking approvals by the Deputy Ministers and Minister”. This second presentation, however, “may be omitted, at the discretion of the Chair, to accommodate unforeseen pressures”.

In the sample examined, we noted that the majority of MCs led by Public Safety Canada were discussed at IPC at least once, while there were only a few instances where MCs led by other government organizations were presented for the committee’s consideration. There were no MCs led by Portfolio Agencies that were approved by Cabinet during the scope of the audit; therefore none were discussed at IPC.

We noted that MCs were either presented at IPC in the early to middle stage of policy development or only prior to seeking approval, but found no evidence of MCs being discussed in conformance with the two-stage approach. IPC members have also confirmed that expectations as it relates to the appropriate timing for presentation to the committee are unclear and that late engagement of the committee has sometimes prevented the members from providing useful and timely feedback on policy proposals. The committee’s secretariat as well as senior management acknowledged that MCs are not always presented to IPC for discussion or are not presented early enough in the policy development stage, and evoked challenges related to tight timelines that may explain the Branches inability to adhere to this step prior to Cabinet presentation.

As such, the scope of the committee could be further defined to reflect the specific expectations as it relates to the timing and nature of MCs that should be presented at IPC. This would contribute to ensuring that Branches present MCs at an optimal time when there can be useful discussions and challenge on policy proposals, and that sponsoring Assistant Deputy Ministers of policy initiatives fully understand their roles and responsibilities as presenters.

Overall, the terms of reference for all internal committees at Public Safety include key elements defining their general purpose; however, the specific mandate, purpose and scope are not clear, both for committees with decision-making authority as well as for those established for consultation or information-sharing purposes. In addition, when reviewed collectively, terms of reference do not follow a common look or use the same terminology. While not a requirement, a consistent structure may contribute to clarity of expectations and support a common understanding of the committees’ responsibilities and accountabilities. Clearly drafted terms of reference contribute to defining intended results and outcomes of a committee and strengthening its culture of accountability.

Communication and understanding of governance bodies’ mandate

To be effective, governance bodies’ mandate, purpose and scope must not only be clearly defined, but clearly communicated to its members. Given that the governance structure should be established in support of the organization’s mandate and priorities, all employees should also be aware or have access to the governance framework established to direct Departmental activities.

We found that there was no formal process in place to inform newly appointed members of the senior management team of their various roles and responsibilities as part of the governance structure. While an Executive Onboarding Program exists and is administered by the Human Resource Directorate, documents distributed as part of this process do not include a comprehensive list of existing governance bodies or the terms of reference of individual committees. Committee members interviewed did not recall receiving information on the internal governance bodies and generally learned of their respective operating procedures through attendance at meetings. That said, members interviewed generally shared a common understanding of the overall expectations for each committee and of the nature of items that should be presented.

Further, the Governance section on the Departmental Intranet is not up to date and includes information on committees that no longer exist (for example, the Departmental Evaluation Committee which was replaced by the PMEC in 2016). During the scope of the audit, there was no information on CCMHR readily available to Public Safety Canada employees on the Departmental Intranet or through the information management system. While it is understood that the mandate of this committee justifies a level of discretion over its specific operations, broad communication of its existence and purpose would contribute to transparency over decision-making authority and accountability in the Department as it relates to human resources management.

2.2 Finding 2: Public Safety Canada has governance bodies in place to support decision-making over all key departmental activities; however, there is no process for regular and overarching review of the governance structure and governance bodies’ terms of reference to support comprehensive oversight and effective decision-making.

The IIA Standards define governance as the “combination of processes and structures implemented by the board to inform, direct, manage, and monitor the activities of the organization toward the achievement of its objectives”. To assess if the governance structure established at Public Safety Canada effectively supports the Department’s overall mandate and expected results, the audit assessed whether the governance bodies have established mandates that provide oversight over all key departmental activities and operate in compliance with their terms of reference. We also assessed whether the structure was reviewed periodically to ensure continued alignment with departmental objectives.

Committees’ oversight over key departmental activities

The audit found that, through their established terms of reference, the governance bodies at Public Safety Canada collectively provide coverage over all key departmental activities. As mentioned above, the documented scope for DMC encompasses a wide range of general management areas, which provides oversight responsibility of all internal services, in addition to responsibility over strategic planning, organizational performance management, and values and ethics. In parallel, IPC is the senior-level management committee responsible for considering key Departmental policy issues and draft MCs, which are developed to support implementation of Public Safety Canada’s Core Responsibilities over emergency management, community safety and national security.

As such, owing to the fact that the committees’ mandate and scope are broadly defined in their terms of reference, Public Safety Canada’s internal governance structure provides for mechanisms that enable senior management to discharge their oversight responsibilities over all key departmental activities. However, as previously mentioned, further clarity over the governance bodies’ mandate, purpose and scope is required.

The audit found that committees within the governance structure were generally operating effectively, that is, in compliance with the expectations documented in their respective terms of reference. Items presented were consistent with the committees’ mandate, attendance at meetings corresponded with committee composition, frequency of meetings was generally followed and decisions/discussions were formally documented and communicated. While, on average, meeting material was not sent to members within the timeframe established in the terms of reference for DMC, DGMC and IPC, committee members interviewed did not raise this as an issue impacting the effectiveness of committee operations (this was not assessed for Excom and CCMHR).

We reviewed agendas, records of decisions, and meeting material to determine whether items presented to committees within the governance structure at Public Safety Canada collectively ensured oversight over key departmental activities. The audit found that the items presented for approval, discussion or information covered a majority of the identified key departmental activities. However, the lack of clarity around the committees’ mandate, purpose and scope results in ambiguity on the specific accountabilities of each governance body. Without a comprehensive grasp of the expected areas for review, there is a risk that the committees may not fully or adequately discharge their oversight role over all management areas.

We found that there was limited coverage of Real Property, Materiel, and Acquisitions Management Services, despite DMC and DGMC responsibilities over these management areas. During the conduct of the audit, senior management acknowledged this gap and recognized that there was a need for a governance mechanism that would provide leadership and oversight for the strategic planning and resource management through the integration of the various departmental plans. This was the impetus for the establishment of the RMC.

The RMC Terms of Reference stipulates that its mandate includes the oversight for the planning and management of the human, real property and asset resources of the Department; therefore, the Terms of Reference of the committee addresses the identified gaps in coverage.

Review of governance framework and committees’ terms of reference

Governance best practices suggest that regular reviews of an organization’s governance framework contributes to mitigating the risk of gap and/or overlap in oversight and to ensuring continued alignment with departmental objectives. Members should regularly discuss and assess individual committee’s performance to identify any impediments to its operational effectiveness and to suggest any areas for improvement. Periodic discussions on the established governance structure also provide an opportunity for senior management to consider whether the decision-making authority is effective and delegated to the appropriate level of the organization.

The audit found that the Terms of Reference for IPC was not reviewed at the frequency established, that the DMC has set out an expectation for its Terms of Reference to be reviewed only every five years, and that CCMHR has not yet set this expectation in its operating procedures. Further, committee secretariat responsibilities are dispersed amongst different directorates and there is currently no joint process within the Department for the review of committees’ terms of reference in support of a comprehensive and integrated governance framework.

The audit also found that, irrespective of the process for individual committees to review the continued relevance of their terms of reference, the scope of committees are not reassessed in light of changes in the operational environment or senior management expectations. For example, the DMC Terms of Reference has not been amended since the establishment of the PMEC in 2016 to clarify the committees’ respective roles and responsibilities with respect to departmental performance management and risk management. Further, despite the inconsistencies between the expected role of IPC for reviewing draft MCs and the operational realities that make it challenging for Branches to do so, the IPC Terms of Reference has not been revised since 2014 to more closely align with senior management needs.

2.3 Conclusion

Public Safety Canada has established governance bodies that operate in compliance with their terms of reference and provide oversight over key departmental activities. However, improvements can be made to clarify elements of the terms of reference and increase effectiveness of the governance structure.

2.4 Recommendation

The governance bodies’ secretariats, at the direction of the committees’ Chair and Members, should establish an integrated governance framework that:

- supports departmental objectives and is reviewed regularly to ensure continued alignment with senior management expectations; and

- is composed of governance bodies that have terms of reference clearly defining the following key elements:

- Mandate

- Purpose, including decision-making authority

- Scope

- Membership/Composition

- Roles and responsibilities

- Quorum requirements

- Frequency of meetings

- Regular review of the terms of reference

2.5 Management Action Plan

| Recommendations | Actions Planned | Target Completion Date |

|

|---|---|---|---|

The governance bodies’ secretariats, at the direction of the committees’ chair and members, should establish an integrated governance framework that: |

|||

|

|

March 2020 | |

|

|

March 2020 | |

Acknowledgements

IAED would like to thank all those who provided advice and assistance during the audit.

Annex A: Audit Criteria

The following criteria were used to ensure sufficient and appropriate testing to support the audit objective and opinion:

| Criterion 1 | The governance structure provides oversight over key departmental activities. |

|---|---|

| Criterion 2 | The mandate, roles, responsibilities and accountabilities of the governance bodies are clearly defined, documented, communicated and understood. |

| Criterion 3 | Governance bodies operate in accordance with their established Terms of Reference. |

| Criterion 4 | Key decisions and relevant information stemming from governance bodies are effectively documented and communicated. |

Footnotes

-

The 10 internal service categories are: Management and Oversight Services; Communications Services; Legal Services; Human Resources Management Services; Financial Management Services; Information Management Services; Information Technology Services; Real Property Services; Materiel Services; and Acquisition Services.

-

The list of 17 areas of management for which DMC is responsible are: Accommodations and facilities management; Asset management; Building emergency management; Business continuity planning; Communications; Contracting and procurement management; Corporate planning and reporting; Federal sustainable development; Information and records management; Information technology management; Investment management; Library and mail services; Management Accountability Framework; Performance measurement; Project management; Risk management; and Security.

- Date modified: